Pricing and Valuing Financial Instruments · 02. février 2025

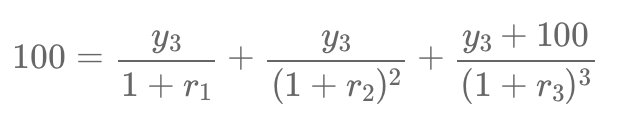

In fixed-income markets, spot rates are crucial for pricing bonds and detecting arbitrage opportunities. However, financial markets typically provide par rates instead of spot rates, making it essential to extract missing spot rates using a process called bootstrapping.

This article explains how to derive spot rates from par bonds, ensuring a no-arbitrage framework.

Pricing et Valorisation d'instruments financiers · 23. septembre 2024

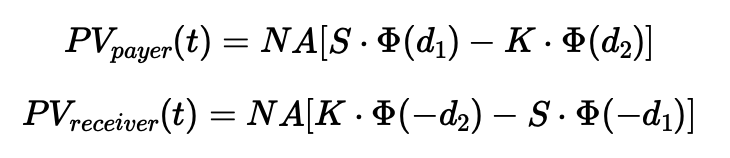

Une swaption est une option permettant d’entrer dans un swap de taux d'intérêt futur, avec deux types : une payer swaption (bénéficiant de la hausse des taux) et une receiver swaption (bénéficiant de la baisse des taux). Utilisées pour la couverture ou la spéculation, les swaptions sont évaluées à l'aide du taux de swap à terme, de la courbe zéro-coupon et de la volatilité implicite.

Mathematical Principles and Quantitative Finance · 19. avril 2024

The trigonometric circle extends complex numbers, useful for visualizing periodic phenomena. In option pricing, the binomial model reflects market uncertainty through a tree structure. Fourier transforms help analyze future payoffs, using the characteristic function of the underlying asset's distribution. Circular convolutions connect binomial models and Fourier transforms, facilitating efficient computation of option prices.

Pricing and Valuing Financial Instruments · 11. novembre 2023

The Jump-to-Default Approach in option trading, modeled by an SDE, highlights how sudden stock price drops (J) affect low strike call options, especially under high credit risk. This contrasts with the Black-Scholes model, which assumes continuous price movements. In high-risk scenarios, the market often lowers the value of these options, factoring in potential defaults, and adjusts implied volatility accordingly. #OptionPricing #CreditRisk #FinancialMarkets #TradingStrategies #InvestmentRisk

Stochastic Models and Processes · 10. novembre 2023

Convertible bonds blend debt and equity, featuring an option to convert into a set number of shares. Key factors include conversion ratio and price. Valuation hinges on stock dynamics, credit risk, and hazard rate. At maturity, value is the higher of face value or conversion outcome. Monte Carlo simulations help in pricing, considering callability and putability options. #ConvertibleBonds #CreditRisk #FinancialModeling #InvestmentStrategies

Functioning of derivatives · 05. novembre 2023

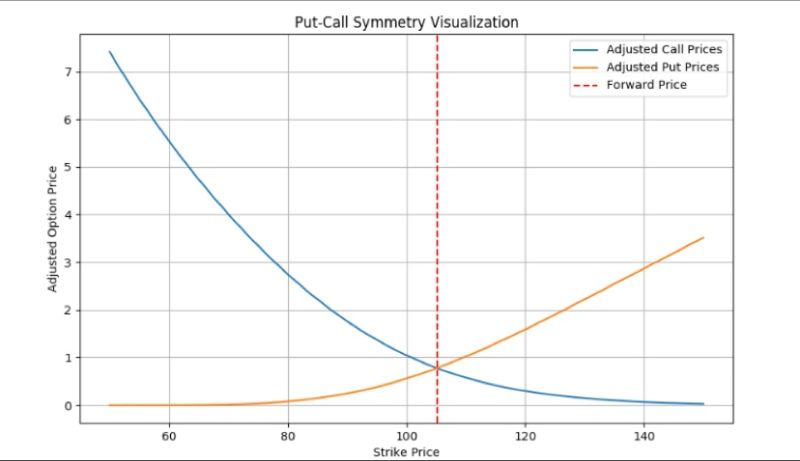

Put-Call Symmetry (PCS) links European put and call option prices via the forward price of the underlying asset. It requires frictionless markets, no arbitrage, zero drift, and symmetric asset returns. PCS is practical for pricing and hedging exotic options, offering a simpler alternative to dynamic hedging by balancing put and call strike prices against the forward price.

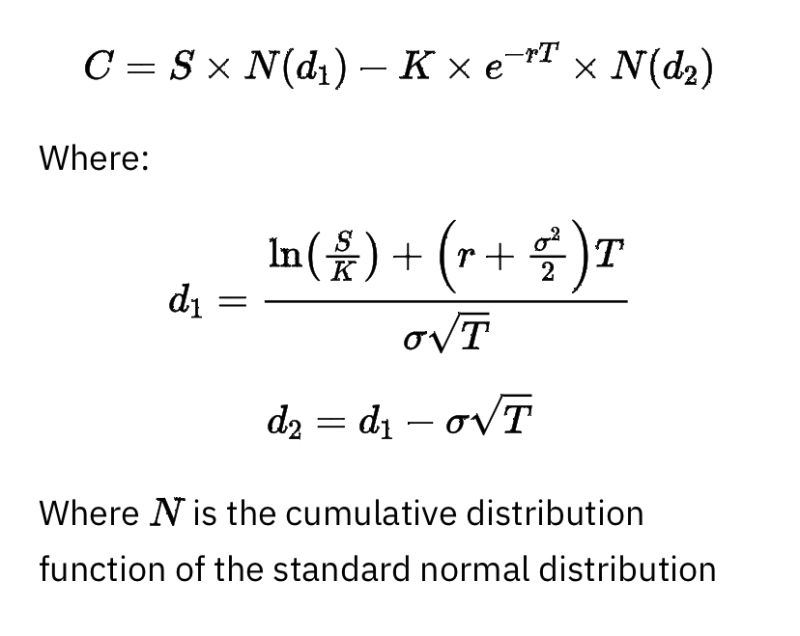

Stochastic Models and Processes · 08. septembre 2023

Unpack the myth that option Delta equals the probability of expiring in-the-money. Dive into risk-neutral valuation and the Black-Scholes model, where assets grow at a risk-free rate, making Delta an unreliable real-world probability indicator. Explore the distinction for smarter option trading. #OptionTrading #BlackScholes #RiskNeutralValuation