Mathematical Principles and Quantitative Finance · 13. novembre 2023

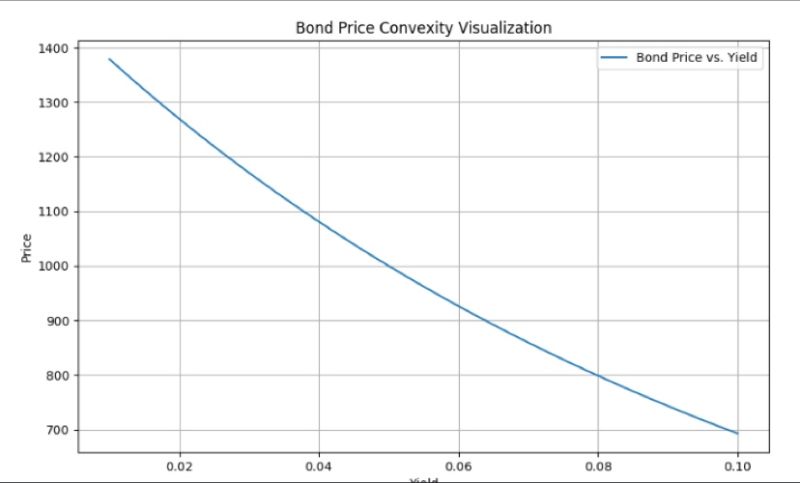

Bond convexity describes the curve-like relationship between bond prices and interest rates, causing prices to rise more when rates drop than they fall when rates rise. This curvature means bond price changes are not linear and convexity corrects pricing models, especially for large rate moves. #BondConvexity