Mathematical Principles and Quantitative Finance · 05. mars 2025

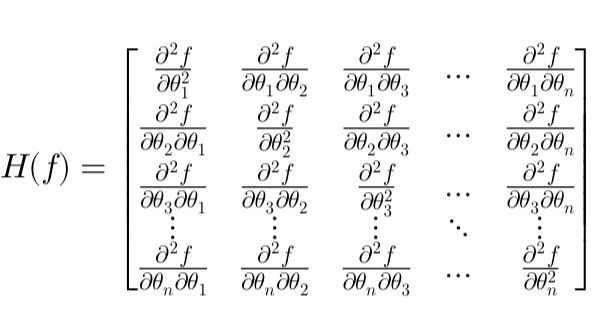

The Hessian matrix, composed of second-order partial derivatives, is a fundamental tool in financial optimization and derivatives pricing. This article simplifies the Hessian’s role in identifying critical points, quadratic approximations, and risk management through Gamma hedging.

Mathematical Principles and Quantitative Finance · 10. janvier 2025

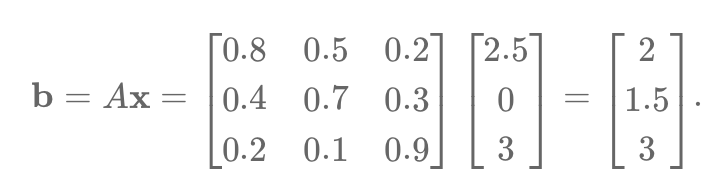

Learn how PCA and SVD simplify financial data by identifying key factors. Discover their role in analyzing relationships between factors (e.g., interest rates) and assets, reducing complexity, and enhancing portfolio management and risk assessment.

Mathematical Principles and Quantitative Finance · 25. décembre 2024

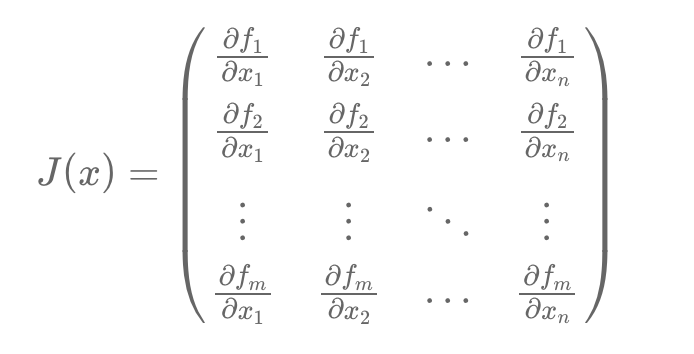

Discover how the Jacobian Matrix plays a crucial role in quantitative finance, from pricing bonds and risk management to sensitivity analysis and yield curve modeling. This article breaks down the mathematical principles behind the Jacobian Matrix and demonstrates its practical applications in analyzing interest rate movements, par rates, and zero rates.